Sales are up, but cash is tight? Learn how an 8–13 week cash flow forecast gives Indian businesses the visibility to stop reacting and start planning.

If we’re brutally honest, most businesses — even well-run ones — struggle to answer two simple questions with confidence:

1. How much do we have to pay our suppliers in the next 30–90 days?

2. How much cash will our customers actually release during the same period?

Ask this in any month-end review, and the room becomes uneasy.

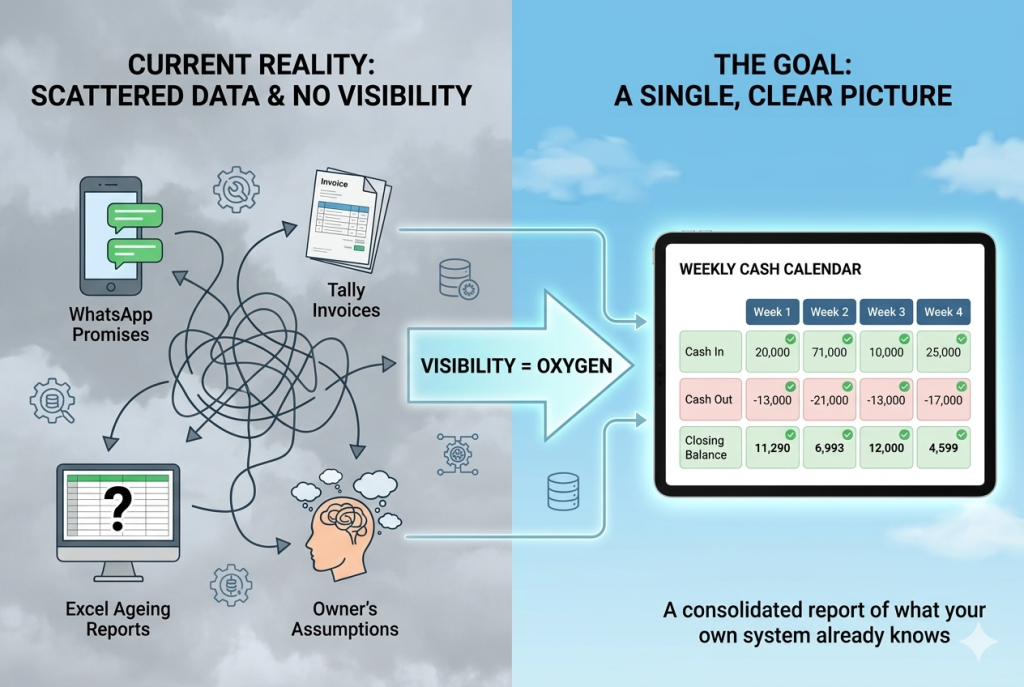

Sales confidently lists expected collections.

Accounts shows pending invoices.

Purchase highlights “urgent” supplier dues.

Finance reminds you that bank limits are tight.

Everyone has pieces of information — but no one has a single, clear picture.

And it’s not because the business is weak. It’s because the information sits everywhere: in Tally, WhatsApp, emails, Excel sheets, and inside people’s heads.

What’s missing is not intelligence.

What’s missing is visibility.

Without knowing who will pay, who must be paid, and when, everything collides — working capital becomes a guessing game.

Businesses don’t fail because they lack profit. They struggle because they can’t see the road ahead.

Why Visibility Is the Oxygen of Working Capital

Working capital problems don’t start with banks, limits, interest costs, delayed customers, or inventory decisions. They start with something far simpler: not knowing what lies in the next 8–13 weeks.

You may have:

- solid sales

- healthy margins

- loyal customers

- efficient operations

…but if the timing of inflows and outflows is invisible, month-end becomes a gamble.

One delayed payment… one bunching of supplier dues… one unplanned raw material purchase… one GST or salary cycle landing in the wrong week… and suddenly the entire month flips.

Visibility ≠ luxury.

Visibility = oxygen.

Without it, businesses don’t manage working capital — they simply survive it, month after month.

How Lack of Visibility Impacts Different Business Models

Cash stress looks different across industries, but the pattern is identical:

Poor visibility → Cash pressure → Bad decisions → Margin erosion.

Bulk raw material purchases go out immediately. Production and collections take weeks. A single dispatch delay triggers discounts, higher OD usage, and deferred purchases — margins fall not from weakness, but from cash timing mismatches.

Fast-moving goods, thin margins, high volume. One large customer paying late — while five suppliers demand payment — can tip a profitable month into a crisis.

Large advances received, then extended expenditure phases. Billing milestones and actual cash arrival rarely align. A single payment delay cascades into delayed salaries and vendor disputes.

Peak procurement in one month, peak sales in another. Without a cash flow map, seasonal businesses routinely run out of credit exactly when they need it most.

The Three Speeds That Drive Your Working Capital

Once you prepare an 8–13 week forecast, you’ll notice something interesting. Your working capital is driven by three speeds:

How fast customers pay you

How long cash stays as stock

How long before you pay suppliers

- Slow customer payments bend the forecast.

- Long inventory days stretch the cash.

- Fast supplier payments tighten liquidity.

Cash Flow Forecasting makes these three speeds visible — sometimes for the very first time. And visibility is what begins improvement.

Cash Forecasting Is Not Difficult. It’s a Coordination Problem.

The formula is simple. The difficulty lies in team coordination. Most ERPs already have payment terms, credit days, supplier due dates, and purchase commitments — but masters are not updated, terms are missing, and data is scattered.

| Team | What They Contribute |

|---|---|

| Sales | Realistic payment expectations and credit terms per customer |

| Purchase | Supplier terms and weekly due lists |

| Stores / Production | Upcoming bulk or advance purchase flags |

| HR | Salary, bonus, and increment timings |

| Finance | Statutory dues, EMIs, interest costs, bank limits |

Pull this into one simple weekly sheet, and “cash forecasting” becomes:

A consolidated view of what your own system already knows.

Most businesses don’t lack tools. They lack coordination and consistency.

Why Organisations Avoid Forecasting: A Behavioural Economics View

People don’t resist forecasting because it’s difficult. They resist it because human behaviour is predictable:

“We’ve survived without it.”

“The customer will pay soon.”

Today’s fire > next month’s crisis.

Fear of being wrong.

Forecasting seems big, so they avoid starting.

Everyone assumes someone else is tracking cash.

Cash flow forecasting isn’t just a finance tool — it is a behavioural intervention. It forces clarity, honesty, and coordination.

How to Start Small (and Choose the Right Method)

Actual cash in / out each week. A simple 8-week cash calendar. Best for getting started immediately.

Profit adjusted for debtor / creditor / stock changes. Better for a management-level view.

Start with the direct method — then grow into 13 weeks, more customers and suppliers, indirect method for management view, and refining accuracy every week.

The goal is not perfection.

The goal is consistency.

Turning Forecasting Into a Habit (Not Just a File)

- ✓One shared sheet, one owner

- ✓20-minute Monday ritual — every single week

- ✓8–13 week rolling window — always forward-looking

- ✓Green / Yellow / Red weeks — colour-coded at a glance

- ✓Review deviations, not people — a learning tool, not a blame tool

- ✓Start with big buckets, add detail later — don’t wait for perfection

Forecasting works when it becomes a rhythm — not an event.

The Real Message: Working Capital Changes When People Change

If there’s one insight this entire journey reveals, it’s this:

Cash stress doesn’t come from low profit — it comes from low visibility.

When a business finally sees its next 13 weeks clearly, decisions become proactive instead of reactive. And from years of working with SMEs, I can say this with conviction:

Cash Flow Forecasting is not a data tool.

It is the first step of working capital management.

It brings every stakeholder — sales, purchase, finance, stores, HR — to the same table, with the same understanding, looking at the same future.

That single act of shared visibility is what starts the journey of working capital optimisation.

Forecasting won’t fix DSO, DIO or DPO overnight. But it will show exactly where the tension lies — and awareness is the beginning of improvement.

How to Improve These Three Speeds Without Breaking Business Relationships

Practical, negotiation-friendly, behaviour-based strategies to reduce DSO, shrink DIO, and extend DPO — without damaging trust with customers or suppliers.

Liquidity Management