Working Capital Series · Part 1

Working capital optimisation for manufacturing

exporters is one of the most misunderstood

concepts in Indian business finance. Every

business owner, in any country, has lived this

scene at least once. Month-end is coming.

Cash is tight. Commitments are not.

THE MONTH-END SCENE EVERY BUSINESS OWNER KNOWS

Salaries are due. GST payment is around the corner. Your bank limit is almost full.

Suppliers are calling: “Sir, payment eppo?”

Your biggest customer politely says: “Sir, next week definitely… please adjust this time.”

Production is asking for more material. The sales team is celebrating a big order.

You look at your sales numbers — they are growing. You look at your bank balance — it is shrinking.

And in that silent moment, you think:

| “Business is running full speed. So why am I always running behind cash?” — The question every Indian business owner asks |

This simple question is the beginning of understanding working capital. Once you understand it clearly, running your business becomes calmer, smoother, and far more predictable.

THE SILENT MISTAKES THAT CREATE WORKING CAPITAL TENSION

Most working capital problems don’t come from one big mistake. They come from small, silent habits inside the company. Here are the most common ones.

| KEY INSIGHT Working capital is not about how much money you have. It is about how fast your money moves through stock, customers and suppliers. |

Thinking Working Capital Means “Cash in Bank”

Real working capital is usually stuck in:

- Stock

- Customers

- Advance payments

| Profit shows up on paper. Cash does not. |

Believing “More Sales = More Cash”

Higher sales often mean:

- More raw material

- More production

- More credit

- More upfront spending

Sales rise. Cash gets tighter.

Leaving Everything to the Finance Team

Sales gives long credit. Purchase pays early. Production builds excess stock.

Then everyone says: “Finance, you manage.”

| Finance handles the outcome, not the cause. |

Treating Inventory Like a “Good Asset”

On the balance sheet, stock looks like an asset. In real life:

| Stock = money sleeping. If it sleeps too long, cash gets stuck. |

Paying Suppliers Too Fast “For a Good Relationship”

Paying suppliers too early may look good emotionally. But it means you use your own money first, even when customers are paying you late.

Assuming Receivables Will Come “Soon”

“Next week” in India can easily become “next month”.

| Loose follow-up and emotional credit decisions slowly choke cash flow. |

All these small habits quietly create working capital tension.

WORKING CAPITAL ISN’T ABOUT CASH — IT’S ABOUT SPEED

Here is the real truth. Working capital is not about how much money you have. It’s about how fast your money moves.

Let’s see it through a dream every business owner secretly has.

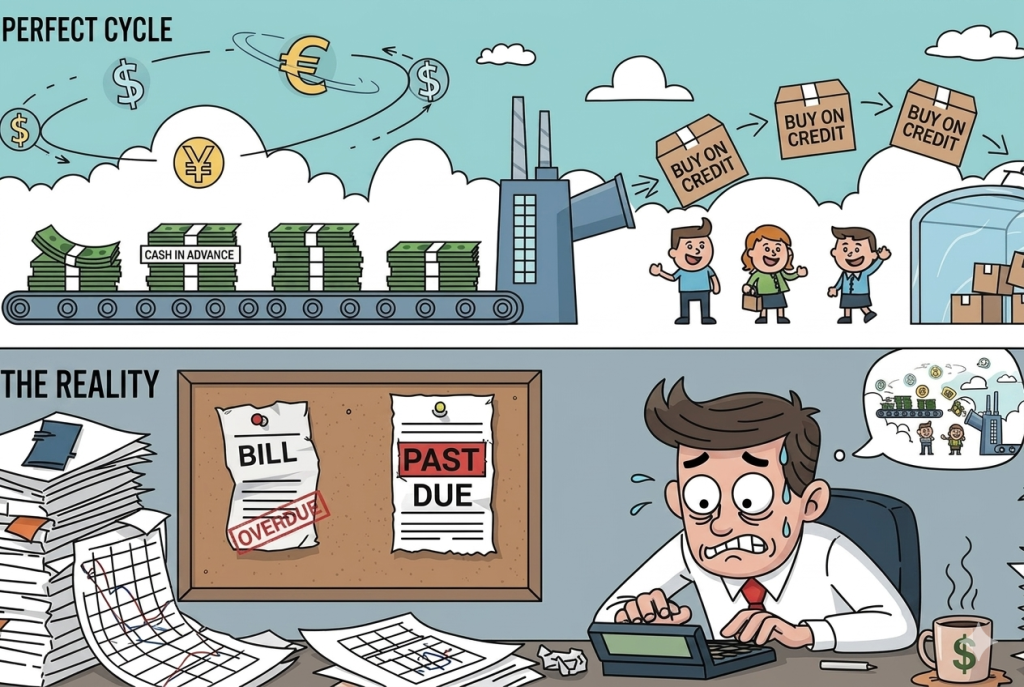

The “Perfect Business” Working Capital Dream

If someone asks: What is your ideal working capital situation? The mind builds a beautiful dream:

- The supplier gives 90 days’ credit

- Goods sell immediately

- The customer pays full cash in advance

You buy on credit, sell instantly, get cash upfront… and pay suppliers after 3 months. No bank limit. No interest. No tension.

At this point, every entrepreneur thinks: “Aaah… ethra manoharamaya nadakatha swapnam” (“What a beautiful dream that will forever remain a dream.)”

The Reality

Real business sounds more like this:

- Supplier: “15–30 days credit only, please don’t delay.”

- Customer: “Next week for sure, sir, please adjust this time.”

- Inventory manager: “Some items are slow-moving, sir.”

- Bank manager: “Sir, utilisation is high, limit tight hai.”

- Accountant: “Sir, GST and salaries are both coming now.”

| The dream is far away. But inside that dream is a very important truth. |

The Real Principle Hidden in the Dream

Even though the dream cannot fully happen, it shows the core rule of working capital management:

- Longer credit from suppliers

- Faster movement of inventory

- Faster collection from customers

This is the golden direction. If suppliers give you more time, your stock doesn’t sit too long, and customers pay quickly — then your business needs much less working capital.

Cash stress drops. Interest cost drops. Bank dependence reduces.

WORKING CAPITAL IS A TEAM GAME, NOT A FINANCE PROBLEM

Working capital is not just a finance topic. It is a company behaviour topic. Your working capital comes from how different teams work every single day.

Sales — The Real Owner of Receivables

Sales decides who gets credit, how many days, what promises are made just to close an order, and how seriously collections are followed up.

| Sales don’t just bring revenue. Sales create receivables — the biggest part of working capital. |

Production / Operations — The Owner of Inventory

Production decides how much to produce, batch sizes, and how much buffer stock to keep. Overproduction = overstock = over-blocked cash. Every extra pallet in your godown is extra money stuck.

Purchase — The Owner of Payables and Raw Material Levels

Purchase influences supplier credit terms, how much you buy, and when suppliers get paid. A good purchasing manager doesn’t think only about price per kg. They think price plus credit plus timing plus quantity.

Finance — The Mirror, Not the Villain

Finance does not create working capital. Finance only measures it and feels the pressure. They are like a thermometer: they show the fever, they don’t cause it.

Owner / CEO — The One Who Sets the Rules

The owner must decide acceptable credit periods, payment discipline to suppliers, how much inventory is okay, and targets for receivable, inventory and payable days. If the owner doesn’t set these rules, each department will follow its own comfort.

| Without clear rules, working capital becomes a tug-of-war. |

THE THREE NUMBERS THAT DECIDE EVERYTHING

Working capital feels complex only until you see it simply. In reality, three numbers decide everything.

| Inventory Days — How many days your money sleeps in stock. If inventory days go up, more cash is stuck in material and finished goods. |

| Receivable Days — How many days your customers take to pay you. If receivable days go up, your customers are using your money to run their business. |

| Payable Days — How many days you get from suppliers. If payable days go up (in a healthy, agreed way), you use their time and their money to support your cycle. |

| Working Capital Cycle = Inventory Days + Receivable Days − Payable Days Example: 40 + 55 − 25 = 70 days of cash locked in your business cycle |

It tells you how many days your money is locked before it comes back to you.

For example: Inventory: 40 days. Receivables: 55 days. Payables: 25 days. Your money is stuck for 40 + 55 – 25 = 70 days. That means your business needs to finance 70 days of activity from your own funds or from the bank.

The Golden Rule

To improve working capital:

- Reduce Inventory Days

- Reduce Receivable Days

- Increase Payable Days (sensibly, not by damaging relationships)

If these three move in the right direction, your working capital improves automatically.

WHEN WORKING CAPITAL WORKS FOR YOU

When working capital is managed well, the whole business feels different.

Salaries Go Out On Time

No more last-minute juggling. Staff feel secure. Morale improves.

Suppliers Trust You

You pay them on time — not too early, not too late. They respond with:

- Better credit terms

- Better prices

- Priority in tight times

This directly helps your working capital.

Customers Respect Your Terms

Because your credit discipline is clear, customers don’t misuse your trust. Receivable days come down. Cash comes in faster.

Inventory Moves, Not Sleeps

Stock is planned. Dead stock is reduced. Your godown becomes a flow, not a storage dump.

Finance Becomes a Partner, Not a Firefighter

With fewer surprises:

- Finance can plan

- Bank negotiations improve

- Interest costs come down

- Projections start matching reality

The Owner Finally Feels in Control

This is the biggest benefit.

- No fear with every unknown call

- No panic at month-end

- No constant stress about ‘limit full’

You can spend more time on strategy and growth, less time on managing shortage.

| When your working capital moves fast, your business becomes peaceful. Inside that peace, growth comes naturally. |

As a continuation of this Working Capital series, upcoming articles will cover cash forecasting, receivables management (DSO), inventory management (DIO), payables management (DPO), and working capital financing. Each topic will focus on practical insights and real-world applications to help improve liquidity and operational efficiency.

| WORKING CAPITAL SERIES — 5 PARTS 1 Sales Are Up, Cash Is Down — Working Capital Simplified (You are here) 2 Cash Flow Forecasting: The First Step in Working Capital Management 3 Receivable Management: How to Bring Your Money Home Faster 4 Inventory Speed: The Cheapest Working Capital 5 The “Pay Late” Trap: Why Your Cash Flow Strategy is Killing Supply |

| FREE TREASURY ADVISORY Is your working capital optimised? In 30 minutes we identify specific opportunities in your cash cycle, banking costs and working capital structure. No obligation. No generic advice. Ever. ► Book a Free 30-Min Treasury Review — fx.fxcapitalindia.in/get-started |